🎙 Smart TVs Now the No. 2 Podcast Device in the UK as Co-Watching Reshapes Audience Measurement

Did someone forward this to you?

Become one of the more than 1000+ valued email subscribers. Find Out More 👈

If you love travel, check out our sister publication “Mencari’s Travel Wire”

👋 Hi, Podsky!

YouTube is eating podcasting’s lunch — and the industry has the data to prove it, ignore it, or finally do something about it. Today’s issue tracks the platform that now commands 13.4% of all U.S. TV viewing, tops podcast discovery at 40%, and leads consumption ahead of Spotify and Apple combined.

Alongside that: Japan opens up for global audio advertisers, smart TVs quietly become the UK’s No. 2 podcast device, and four audio trade bodies show up to Cannes Lions with 17 years of profit data that every podcast sales team should have memorised by Monday.

If this is your first time here, welcome. Over 1,000 podcast industry readers already call Podwires home. Join them here.

Independent media only works when communities back it. Subscribe, share, and support the creators in your corner—starting with a Podwires paid subscription that keeps this newsroom running.

We want everyone to know about this initiative, so please spread the word by sharing the email with your friends! (copy URL here)

And, as always, send us feedback at editor@podwires.com

Big week. Let’s get into it.

Today’s reading time is 5 minutes. - Miko Santos (June 27, 2026)

🎙️ Today, we have exclusive insights on:

Japanese Market Entry Just Got Easier for Global Podcast and Audio Ad Players

YouTube Claims 13.4% of All U.S. TV Viewing in April, Widening Lead Over Every Rival Platform

Audio Lifts Campaign Profit by 75%, Global Study Finds as Industry Bodies Unite at Cannes Lions

Podcast Insight: Smart TVs Now the No. 2 Podcast Device in the UK as Co-Watching Reshapes Audience Measurement

PodBusiness: YouTube Tops Podcast Discovery and Consumption as Social Platforms Claim 61% of How Listeners Find New Shows

OTONAL

Japanese Market Entry Just Got Easier for Global Podcast and Audio Ad Players

Podwires Rundown: Japan has long been the elusive target for audio advertising expansion. Big economy. Sophisticated media market. Enthusiastic digital audience. And a language that will absolutely punish a lazy translation job. Otonal Inc., a Tokyo-based digital audio advertising and podcast technology company, is betting it can solve that last part — and the launch couldn’t be better timed.

The company just officially rolled out a specialised audio localisation service built specifically to help global brands and media companies adapt English-language podcasts and audio ads for Japanese listeners. This isn’t a text translation play dressed up in audio clothing. Otonal is rebuilding the whole thing from the ground up: scripts rewritten for spoken Japanese, strict 15- and 30-second ad timing precision, culturally adapted content, and native Japanese voice talent sourced through FM BIRD, Otonal’s own talent agency specialising in radio personalities and narrators.

Here’s the uncomfortable part the industry often skips past: Japanese isn’t just difficult to translate. It’s structurally different in ways that break audio formats. Call-to-actions land at the end of sentences. Politeness registers shift meaning. Emotional flatness in a literally accurate translation can ruin a campaign before it even starts. Otonal CEO Taisuke Yagi put it plainly: audio spots live in seconds, not pages. A sentence that reads correctly on paper can feel stiff and confusing out loud.

Otonal has planned over 4,500 digital audio campaigns and supported more than 1,500 advertisers in Japan. That’s not a startup pitch — that’s operational credibility in a market where most overseas players are still trying to figure out where to start.

The service is also deliberately built for non-Japanese-speaking global and APAC teams, with English-first project management, back-translations, and explanatory notes so overseas approvers actually understand what they’re signing off on. That’s a detail worth pausing on. Most localisation vendors hand you a finished audio file and a prayer. Otonal is building in transparency checkpoints. Smart.

The Key Points

Japan ranks among Asia’s largest advertising markets and its digital audio ecosystem is growing rapidly — making it a high-value, high-barrier opportunity for international brands

Otonal has planned 4,500+ digital audio campaigns and worked with 1,500+ advertisers in Japan, giving the new service a meaningful operational foundation

The service goes beyond translation — scripts are rebuilt for spoken Japanese rhythm and timing, not just converted word for word.

English-first project management is built in, with back-translations and approval checkpoints designed for global teams who don’t speak Japanese

Voice talent comes from FM BIRD, Otonal’s own agency specializing in radio personalities and narrators — giving the service a production-grade edge over generic freelance casting

Why It Matters

Japan is one of those markets everyone in global audio talks about but few have cracked. The language barrier isn’t just about vocabulary — it’s about how spoken Japanese works differently than written Japanese, and how both work differently than English. Most localization attempts fail not because the words are wrong but because the sound is wrong. Otonal is attacking that specific problem with infrastructure that already exists — campaigns planned, advertisers managed, talent agency in-house. For any podcast network or audio ad platform eyeing Asia Pacific expansion, this is a meaningful new on-ramp.

The Big Picture

For podcasters: If you’re producing English-language content with any aspiration towards Asian market reach, Japan is a natural first stop — and previously, it was a very expensive, very opaque one. A service like this lowers the barrier considerably. The actionable move here: assess whether your top-performing episodes have cross-cultural resonance before committing to localisation spend. Not every show translates. The ones that do – interview formats, business, true crime, and narrative – now have a clearer path to one of the world’s most engaged digital audio audiences.

For podcast producers: This is a workflow inflection point. Localising audio content isn’t just a translation task — it’s a production task. This includes script reconstruction, timing alignment, voice direction, and platform delivery. Producers who develop fluency in localisation workflows, or who build relationships with vendors like Otonal early, are positioning themselves for a genuinely differentiated service offering as clients start asking the question: “Can we take this to Japan?”

For the industry: The global audio advertising market has been talking about Asia Pacific as the next growth frontier for years. What’s slowed it down isn’t appetite — it’s infrastructure. Otonal’s move signals that the infrastructure layer is being built. Watch for similar services to emerge across South-east Asia. The podcast industry’s next phase of international growth won’t just rely on platform algorithms. It will be driven by localised capabilities. This is what it looks like when it starts.

TOGETHER WITH MENCARI TRAVEL WIRE

Your Next Adventure Starts Here

Mencari Travel Wire is the go-to travel newsletter for Australia and New Zealand — delivering destination guides, travel intel, and trip-planning essentials curated for readers who move with purpose. Whether you're chasing weekend escapes or planning your next big journey across the Tasman, we've got you covered.

Subscribe Free → TRAVEL WIRE

This section is a paid advertisement. If you are interested in advertising, let’s talk.

NIELSEN

YouTube Claims 13.4% of All U.S. TV Viewing in April, Widening Lead Over Every Rival Platform

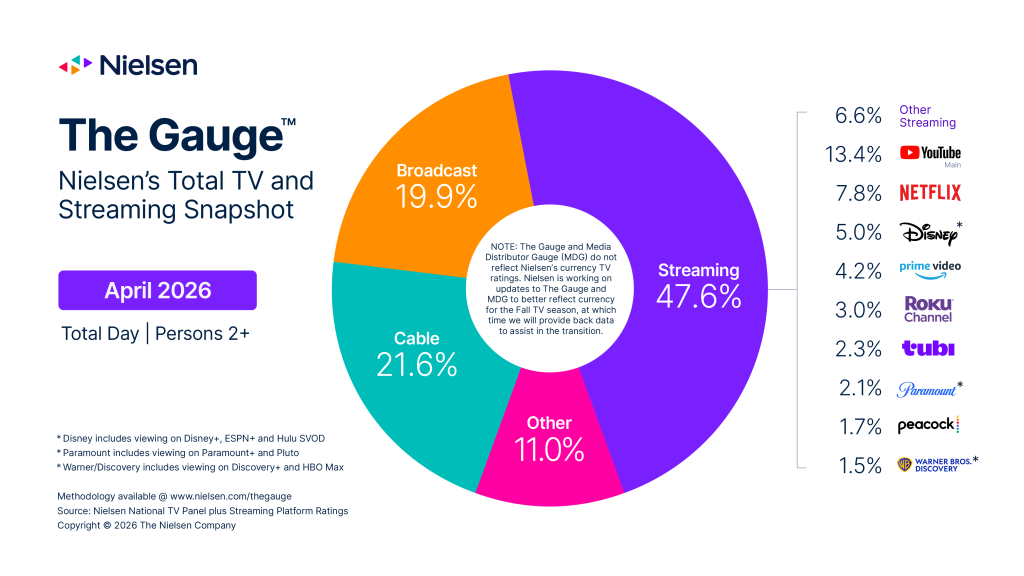

Podwires Rundown: Look at this number and let it sit for a second: 47.6%.

Streaming commanded 47.6% of all TV watch time in April 2026, according to Nielsen’s latest Gauge and Media Distributor Gauge reports. Nearly half of everything Americans watched on their televisions last month came from a streaming platform. Cable — which everyone has been burying for years — actually gained share for the second consecutive month, but still only managed 21.6%.

And sitting at the very top of that streaming mountain? YouTube. Again.

YouTube maintained its No. 1 position in Nielsen’s Media Distributor Gauge with 13.4% of total TV watch time in April, adding 0.2 points to its share. Less than 13.4% of streaming. Thirteen point four per cent of all television watch time. Every cable channel, every broadcast network, every streaming competitor — YouTube beats them individually. And it’s not even close.

The awkward thing here is: YouTube is not a podcast platform. It’s a video platform that happens to have a lot of podcast material. The audience that’s watching Joe Rogan or Call Her Daddy or any number of top podcast properties on their living room TV on YouTube? Nielsen counts those as YouTube views. Not listening to poadcasts. No sound listening. YouTube’s victory.

Is YouTube? The report covers the four-week interval from March 30 through April 26, 2026, a period also shaped by the NCAA Basketball Tournament conclusion, the Masters golf tournament, and the start of the NBA Playoffs. Sports events drove significant cable and broadcast engagement — but even event-driven live sports couldn’t knock YouTube off the top of the streaming rankings.

The other number worth flagging for the podcast industry: Amazon Prime Video climbed to 4.2% of TV in April, a gain of 0.4 points, boosted significantly by its slate of 22 NBA games, including Play-In Tournament and Playoff coverage. Amazon is buying live sports rights and it’s paying off in shares. Meanwhile, Tubi reached a platform-best 2.3% share of television – the highest in its history – by doing it with entirely free, ad-supported content.

REALLY? Yes. Really. The free ad-supported streamer is hitting record numbers while podcast publishers are still debating whether to put their shows on YouTube.

Source Note: Data sourced from Nielsen’s April 2026 Gauge and Media Distributor Gauge reports, published June 25, 2026. Nielsen is a commercial audience measurement company with a commercial interest in demonstrating the value of its measurement products. The Gauge figures reflect total TV viewing and include both ad-supported and non-ad-supported consumption. Nielsen has noted it is working on updates to align Gauge reporting with recent February 2026 currency ratings enhancements; some data comparability limitations apply.

The Key Points

Streaming reached 47.6% of total U.S. TV watch-time in April 2026 — effectively claiming half the television audience

YouTube holds 13.4% of all TV viewing, maintaining its No. 1 position in Nielsen’s Media Distributor Gauge for another consecutive month

Cable gained 0.2 share points to reach 21.6% — its highest six-month result — driven primarily by the NCAA Men’s Basketball Championship on TBS/TNT/TruTV

Amazon Prime Video climbed to 4.2% share on the back of 22 NBA games, demonstrating that live sports rights are a direct share accelerant

Tubi hit a platform-record 2.3% share, proving the ad-supported, free streaming model is still growing in a crowded market

Why It Matters

Every minute an audience spends on YouTube counts toward YouTube’s share of television. Not audio’s share. Not podcasting’s share. YouTube’s. For the podcast industry, this Nielsen report is less about who won April TV and more about where the audience’s media diet is being measured — and who captures the credit. As more podcast content migrates to video and lands on YouTube, the medium gains reach but loses identity in the data. The audience is there. The attribution isn’t. Understanding how the total TV pie is being divided — and how fast streaming is consuming it — is foundational intelligence for any podcast executive thinking about distribution, advertising, or platform strategy in 2026.

The Big Picture

For podcasters: YouTube at 13.4% of all TV is not an abstraction. It is your distribution reality. If your show doesn’t have a YouTube presence, you are absent from the platform that commands more television watch time than any individual cable or broadcast network. Actionable move: audit your YouTube strategy today. Not for virality. For share. For discoverability. For the audience that now watches podcasts on their televisions the same way they used to watch cable.

For podcast producers: The Tubi story is worth watching closely. An ad-supported free streamer just hit record share by leaning into volume, availability, and zero friction. That’s the FAST channel playbook — and it’s working. Producers who understand how to package catalogue content and long-form interview programming for FAST distribution are sitting on an underutilised asset. The model exists. The audience exists. The infrastructure question is whether your content is formatted and licensed to take advantage of it.

For the industry: Nearly half of all television viewing is now streaming. Broadcast and cable — the two categories that podcast advertising has historically benchmarked against for audio ad spend justification — are below 42% combined. Podcast sales teams are pitching against a competitive media landscape that is being redrawn in real time. Audio reach arguments must account for a world in which the living room TV is increasingly a YouTube and streaming device. The industry’s measurement frameworks, CPM benchmarks, and advertiser conversations need to catch up to what Nielsen is reporting every single month.

PRESENTED BY PODWIRES MARKETPLACE

Build Better Podcasts With Podwires

Every great podcast needs the right team behind it. Podwires is a dedicated marketplace where creators can connect with skilled podcast producers, editors, and audio professionals who understand how to shape strong, polished shows.

Built for the podcast industry, Podwires brings together talent, opportunity, and visibility in one clean platform. Whether you are launching a new show or improving an existing one, Podwires helps you find creative partners who can make your production stronger.

Podwires connects clients with top independent podcast producers and freelancers through a dedicated marketplace built for audio work.

SIGNAL HILL INSIGHTS

Smart TVs Now the No. 2 Podcast Device in the UK as Co-Watching Reshapes Audience Measurement

Podwires Rundown: Let’s talk about something the podcast industry keeps dancing around but hasn’t fully absorbed yet.

The living room is a podcast platform now.

Not metaphorically. Not aspirationally. Currently, in the UK, nearly half of monthly podcast consumers watched a podcast on a smart TV last month. The device once used for Netflix and football is now a primary surface for podcast content. And it’s doing something podcast executives should pay attention to: it’s pulling in more than one viewer at a time.

Smart TVs are now the second most-used device for consuming podcasts in the UK, with 45% of monthly consumers having used one for podcasts in the past month. Smartphones still lead at 80% — that’s not surprising. But smart TVs have leapfrogged computers and tablets. Let that sink in.

Here’s where it gets genuinely interesting for advertisers and publishers: 42% of smart TV podcast watching happens with someone else — co-watching. Smart TVs account for just over half, 52%, of all podcast watch time. Co-watching. That’s not a download. That’s not a stream. That’s a multiplier. One view, potentially two pairs of ears. The industry has been obsessing over download numbers and unique listeners. The smart TV is quietly making those metrics incomplete.

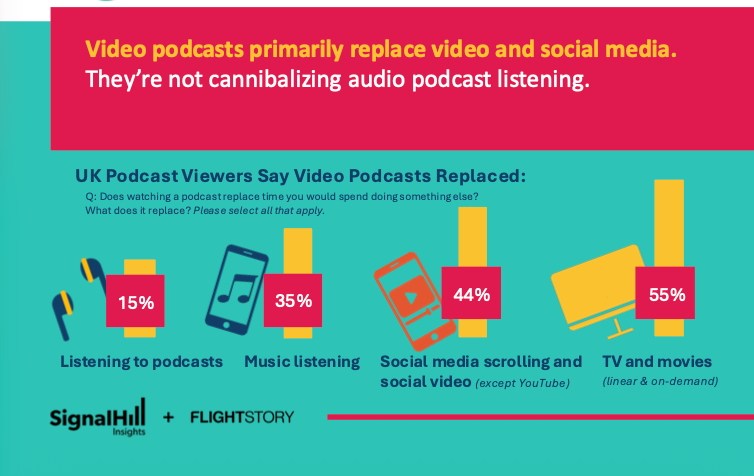

The vast majority — 84% — of monthly podcast consumers in the UK watched a podcast in the last month, while 90% listened to one. Video podcasts primarily replace TV, movies, and social media scrolling. They are not cannibalising audio podcast listening. Only 15% of UK podcast viewers say watching replaced time they would have spent listening to podcasts. Is the fear that video eats audio? Not supported here.

The time-of-day data is where the strategic implications really crystallise. 54% of consumers watch video podcasts during weekday evening prime time — more than any other time of day. Listening, by contrast, is more evenly distributed throughout the day, with less disparity between AM and PM. Video podcasting is a primetime play. Audio podcasting is an all-day companion. These are different products serving different moments — and smart publishers will plan their distribution, ad placement, and content strategy accordingly.

When comparing the smart TV podcast experience to smartphones, consumers are much more likely to say the smart TV experience is better rather than the same or worse. 36% describe it as more premium, and 43% say it is more engaging or more convenient. Fewer than 10% describe it as less engaging, less convenient, or inferior.

More premium. That’s the phrase advertisers should highlight to their planning teams.

Young people are driving smart TV adoption, with 64% of 18-to-34-year-olds using a smart TV for podcasts in the last month. This demographic is the audience every brand is chasing. And they’re watching podcasts on the biggest screen in the house.

Source Note: This report — Podcasts in the Living Room UK, 2026 — was produced by Signal Hill Insights in partnership with Flight Story, a content and media company with a commercial interest in the growth of video podcasting. The survey was conducted using a nationally representative panel of 1,003 monthly podcast consumers aged 18 and over in the UK, fielded between March 3 and 9, 2026. Signal Hill Insights is a paid research services firm; this study was commissioned rather than independently funded. The sample is limited to existing monthly podcast consumers, not the general population, meaning figures on watch rates and device usage reflect an already-engaged audience – not total market penetration. Treat reach projections with appropriate caution.

The Key Points

Smart TVs are the #2 podcast device in the UK, used by 45% of monthly podcast consumers in the last month — overtaking computers and tablets

84% of UK monthly podcast consumers watched a podcast in the last month; 90% listened — a gap of just 6 percentage points

52% of all podcast watch time in the UK happens on smart TVs, and 42% of that is co-watched with at least one other person

54% of video podcast viewing happens during weekday evening prime time — directly competing with linear TV and on-demand streaming for the same eyeballs, in the same room

Video podcasts are replacing TV, movies, and social media scrolling — only 15% of viewers say it replaced audio podcast listening

Why It Matters

The UK podcast audience is telling the industry something it needs to hear: the living room is not a secondary screen for podcasts — it’s becoming a primary one. This changes everything from ad format strategy to production investment to how publishers pitch reach to advertisers. A co-watched smart TV episode is a fundamentally different audience proposition than a solo listen on earbuds during a commute. The industry has pricing models, attribution tools, and measurement frameworks built for the latter. The UK data suggests it’s time to build the infrastructure for the former. And if the UK is any guide to where other markets are heading — and it historically has been — the rest of the world is about 18 months behind this curve.

The Big Picture

For podcasters: The primetime finding is actionable right now. If your show has video, it is competing with Netflix and linear TV between 7pm and 11pm — not just other podcasts. That reframes your value proposition to advertisers completely. A video podcast airing in a UK household’s evening isn’t background content. It’s lean-forward entertainment. Actionable move: start thinking about your show’s visual quality not just for clips and YouTube thumbnails but for a 55-inch screen viewed from a sofa. Set design, guest framing, and production quality now matter in a TV-grade way.

For podcast producers: Co-watching changes the unit economics of audience building in ways the industry hasn’t fully priced in. If 42% of smart TV podcast time involves more than one viewer, then the effective reach of a well-produced video episode is materially higher than download or unique listener figures suggest. Producers who can articulate this to clients — and who can design content that holds attention in a shared-screen environment — are offering something genuinely differentiated. Start building co-viewing into your pitch decks.

For the industry: The measurement gap is getting embarrassing. The podcast industry is still largely selling audio reach while a significant and growing portion of consumption is happening on the biggest screen in the home, often with more than one person watching, during the same primetime window that television has charged premium rates for decades. The Signal Hill/Flight Story data gives the industry the language it needs to have a different conversation with media buyers. The question is whether the trade bodies, measurement vendors, and major publishers will move fast enough to capture the opportunity — or whether YouTube and connected TV platforms will take the revenue credit for the audience that podcasting built.

Podwires x PodRoo

Podwires is excited to welcome PodRoo as a new partner.

PodRoo is a free press release platform built specifically for the podcasting community, helping hosts, guests, agencies, and producers share their news with the right audience.

Whether you’re announcing a new show, a milestone episode, a guest appearance, or a sponsorship deal, PodRoo makes it easier to get in front of podcast listeners, industry insiders, and media outlets that follow the space.

We’re proud to partner with platforms that support podcast growth, visibility, and discovery.

Check out PodRoo at PodRoo.com.

SOUND PROFITABLE | JAR PODCAST SOLUTIONS

YouTube Tops Podcast Discovery and Consumption as Social Platforms Claim 61% of How Listeners Find New Shows

Podwires Rundown: Let’s be direct about what this research is actually saying.

Podcast discovery has moved. It moved a while ago. And most of the industry is still optimising for a world that no longer exists.

Sounds Profitable and branded podcast agency JAR Podcast Solutions surveyed podcast listeners and found that 40% discovered their favourite podcast on YouTube — more than double any other tested channel. When you add Facebook, TikTok, and Instagram to the mix, 61% of listeners say they found their favourite show on YouTube or social media. Sixty-one percent.

Meanwhile, the industry has spent years refining trailer strategies, sweating chart rankings, and cross-promoting inside podcast apps to an audience that was already there. The people who weren’t already there — the ones actually growing the medium — found their way in through a YouTube search, a TikTok clip, or a post from someone they follow.

Here’s the other finding worth sitting with. Among listeners who discovered a podcast through social media, 60% found it through organic content shared by someone they follow. Not ads. Not sponsored posts. Someone they trust shares something they loved. Only 33% attributed discovery to sponsored content.

The industry has been buying its way to discovery. The audience has been trusting its way there.

On consumption, YouTube isn’t just winning at discovery. 40% of listeners identified YouTube as their most-used podcast platform — ahead of Spotify at 18% and Apple Podcasts at 11%. YouTube is not a feeder channel anymore. It’s the main event for a substantial portion of the podcast audience.

Fair play to the platforms that still hold real cards. Spotify-discovered listeners are among podcasting’s most engaged, with 61% listening weekly. Apple Podcasts browsing continues to drive discovery among affluent, audio-first listeners — particularly in news and technology. TikTok discovery skews dramatically young: it’s nearly seven times more common among listeners 18–34 than those 55 and older. And host recommendations, though a smaller share of overall discovery, still deliver the highest concentration of super-fans.

The word-of-mouth data is also significant. 64% of podcast listeners receive recommendations from friends, family, or colleagues, and 72% say they’re likely to act on those recommendations. Personal trust remains the most potent discovery mechanism in podcasting — YouTube and social just happen to be the infrastructure that scales it.

For advertisers, the research surfaces something worth flagging: brand-produced podcasts generated a +27-point net lift in trial intent overall, with higher performance among highly engaged audiences. Listeners are more receptive to branded podcast content than most marketing teams assume. That’s not a small number.

Source Note: This research was produced by Sounds Profitable, a trade association for the podcasting industry with a stated goal of growing advertiser investment in podcasting, in partnership with JAR Podcast Solutions, a branded podcast agency with a direct commercial interest in the growth of branded podcast content. Both organisations benefit from findings that validate podcast investment and social/YouTube distribution strategies. The full methodology — including sample size, fielding dates, and panel composition — is available in the complete report at soundsprofitable.com. As with all industry-commissioned discovery research, you should read the results as indicative of directional trends rather than definitive population-level benchmarks.

The Key Points

40% of podcast listeners discovered their favorite show on YouTube — more than double any other single source tested

61% of listeners found their favorite podcast through YouTube or social media combined, making these platforms the dominant discovery ecosystem for the medium

YouTube is also the most-used podcast platform at 40%, surpassing Spotify (18%) and Apple Podcasts (11%) for consumption – not just discovery

60% of social-media-driven discovery came from organic content shared by someone the listener follows, versus 33% from sponsored posts

Brand-produced podcasts delivered a +27-point net lift in trial intent, suggesting listener receptivity to branded content is higher than marketers typically assume

Why It Matters

Discovery is the unsolved problem of podcasting. Always has been. The industry built brilliant content and then asked audiences to locate it inside apps designed primarily for people who already listen to podcasts. This research confirms what many suspected but few had data to support: the audience that’s actually growing in podcasting is entering the medium through YouTube, TikTok, Instagram, and personal recommendations — not through app store charts or cross-promotional spots. That has direct implications for how publishers allocate marketing budgets, how producers approach clip strategy, and how advertisers evaluate platform mix. If you’re measuring podcast campaign success without accounting for YouTube-driven discovery, you’re working with an incomplete picture.

The Big Picture

For podcasters: The discovery data is a direct brief for your content strategy. If 60% of social-driven discovery comes from organic shares rather than paid promotion, your best marketing asset is a moment in your show compelling enough that someone shares it unprompted. That’s a production and editing challenge as much as a marketing one. Actionable move: audit your last 10 episodes for the three-to-five-minute clip that would make a new listener stop scrolling. If you can’t identify one, that’s your content gap. Build towards that moment intentionally and then put it on YouTube — not just as a full episode, but as a standalone piece worth discovering.

For podcast producers: The platform-specific audience profiles buried in this research are a client briefing in disguise. TikTok audiences are young and diverse. Spotify-discovered audiences listen weekly and respond well to brand content. Apple Podcasts audiences skew affluent and are audio-first. These are not the same listeners — and you shouldn’t target them the same way. Producers advising clients on launch strategy need to ask a foundational question before recommending any distribution plan: who are we actually trying to reach, and where are they already spending time? The days of “distribute everywhere and optimise later” are over. Channel-specific strategy is now a baseline expectation.

For the industry: The +27-point branded podcast lift number is the figure trade bodies and publishers should be putting in front of every CMO conversation. Branded podcast scepticism has always partly stemmed from the assumption that listeners resist content produced by brands. This research pushes back on that directly. Combined with the data on YouTube’s dominance in discovery, it builds a coherent case: the audience is on YouTube, they’re receptive to brand content, and word-of-mouth scales it organically. That’s not a niche pitch anymore. That’s a mainstream media strategy argument.

CRA

Audio Lifts Campaign Profit by 75%, Global Study Finds as Industry Bodies Unite at Cannes Lions

Podwires Rundown: Here’s a number that deserves to be on every podcast advertising pitch deck produced in the second half of 2026.

+75%.

That’s the profit uplift for campaigns that include audio versus those that don’t. Not reach. Not awareness. Profit. This is the metric that CFOs actually care about.

The audio industry bodies of Australia, the UK, Ireland, and the United States just did something they’ve never done before: they showed up to Cannes Lions together, with a unified dataset, and made a single global argument. Commercial Radio & Audio (CRA), Radiocentre UK, Radiocentre Ireland, and the Radio Advertising Bureau US brought Professor Mark Ritson to present findings drawn from the Effie x System1 global databank — 1,262 campaigns, 17 years of data, spanning four markets. The session, titled The Secret to Profit and Trust: Audio, played to a standing-room-only crowd.

Let that image sit for a second. Standing room only. At Cannes Lions. For an audio session.

The headline numbers are significant. Campaigns with audio outperform those without on profit (+75%), trust (+81%), price insensitivity (+81%), and customer acquisition (+19%). Across 14 commercial measures, the average uplift for all campaigns with audio was +22% compared to campaigns without. And the profit contribution scales with media spend — meaning the more you invest in audio, the more it compounds.

Here’s the uncomfortable part for anyone who’s spent the last five years treating audio as a must-to-have line item in a video-heavy media plan: you’ve been leaving money on the table. Provably. With 17 years of data.

The creative finding is where it gets even more interesting for podcast publishers. Audio nearly doubles the profit generated by emotionally driven campaigns. And when you pair audio with distinctive brand assets and run it consistently over time, the effect compounds again. Podcasting — with its intimate host-listener relationship, high-trust environment, and parasocial dynamics — is arguably the most emotionally potent audio format in the mix. This research doesn’t say that explicitly. But the implication is particularly pronounced to miss.

Ritson called it “beautiful data” and described audio as “the catalyst that makes your whole campaign work harder.” The CRA’s CEO Lizzie Young, noted that a case first built on Australian Effie data now holds across the UK, US, and Ireland — suggesting the audio effectiveness premium isn’t a quirk of one market. It’s structural.

The original study was commissioned in Australia, where CRA analysed Effie effectiveness data with independent marketing consultant Rob Brittain and Ritson. That modelling has since been tested against a new global databank and has been confirmed. The global collaboration itself is the strategic story. These four industry bodies have historically operated in isolation, each making market-specific cases to market-specific advertisers. Showing up together at the world’s most influential marketing conference with unified global evidence is a different kind of play.

Source Note: This research was presented by Commercial Radio & Audio (CRA), Radiocentre UK, Radiocentre Ireland, and the Radio Advertising Bureau US — all industry trade bodies with direct commercial interest in increasing advertiser investment in audio. The Effie x System1 Databank provides the data, covering 1,262 campaigns from 2007 to 2023 across the UK, Ireland, Europe, and the US. System1 is a commercial creative effectiveness platform with its own commercial relationship with advertisers. While the Effie database is a respected industry source, parties with a stake in the outcome commissioned and framed the analysis. The findings should be read as strong directional evidence rather than independent academic research. The campaign period (2007–2023) predates the current scale of podcast advertising, meaning audio’s contribution is likely weighted toward broadcast radio rather than podcast-specific placements.

The Key Points

Campaigns with audio outperform those without on profit by +75%, trust by +81%, price insensitivity by +81%, and customer acquisition by +19%

Average uplift across 14 commercial measures was +22% for campaigns that included audio versus those that didn’t — and the contribution scales with media spend

Audio nearly doubles the profit of emotionally driven campaigns, with the effect compounding further when paired with distinctive brand assets and consistent scheduling

The dataset spans 1,262 campaigns across 17 years (2007–2023), tested across Australia, the UK, Ireland, and the US – making this the broadest cross-market audio effectiveness study presented to date

Four audio industry bodies united for the first time at Cannes Lions to present a coordinated global case for audio’s role in the media mix – a strategic escalation in how the audio industry advocates for itself

Why It Matters

The podcast advertising industry has been making qualitative arguments about intimacy and trust for years. This dataset gives the industry a quantitative backbone. A +75% profit uplift is not a brand awareness story — it’s a business outcomes story. That’s the language media buyers respond to, and it’s the language CMOs need when they’re defending audio investment to CFOs who want performance metrics. The fact that this evidence now holds across four markets simultaneously removes the “that’s just how it works in one country” objection. For podcast publishers and audio ad sellers in Australia, the UK, and beyond, this research is a ready-made business case. The work now is connecting the broadcast audio effectiveness data to podcast-specific placements — which the research doesn’t do directly, but which the industry needs to do urgently.

The Big Picture

For podcasters: The +27% branded podcast trial intent lift from the Sounds Profitable research earlier this week, stacked against the +75% profit uplift from this Cannes Lions dataset—these two numbers, read together, are a compelling advertiser brief. Podcasting offers the emotional intimacy that audio effectiveness research identifies as the profit multiplier, delivered at scale, with measurable attribution. The industry has the data. The gap is in how podcast publishers are packaging and presenting it. If you’re running a show with a loyal, engaged audience and you’re not actively pitching advertisers with effectiveness language — profit, trust, price insensitivity — you’re underselling the product.

For podcast producers: Production consistency matters more than this research is given credit for. The compounding effect of running audio with distinctive brand assets consistently over time is a direct argument for long-term branded podcast partnerships over one-off sponsorship deals. Producers who can build the case for 12-month brand integrations — rather than four-episode test buys — are doing work that this effectiveness data supports. The data says consistency compounds. Build your client proposals accordingly.

For the industry: The coordination play at Cannes Lions is the real strategic development here. Four industry bodies, one global stage, one unified dataset. That’s a lobbying and advocacy shift the podcast industry should watch closely. Broadcast radio has historically been better organized in its advertiser conversations than digital audio. If that coordination extends to include podcast-specific effectiveness data in the next iteration of this research — and it should — the industry will have a cross-format, cross-market effectiveness argument that competes directly with video on its own terms. The audio industry has just demonstrated its ability to take a long-term view. The podcast industry needs to be in the room when the next dataset is built.

EDISON RESEARCH

UK's Top Podcasts Publish 11 Episodes Monthly and Drop on Wednesdays — But Growing Shows Shouldn't Copy Their Metadata

Podwires Rundown: There’s a trap buried in every “what the top shows do” study. And to their credit, Ausha and Edison Research actually name it – before promptly stepping around it.

Here’s the trap: the habits of the most successful podcasts in any market are partly what made them successful and partly what they can afford to do because they’re already successful. Those two things are not the same. Copying the metadata brevity of a show with eight and a half thousand Apple Podcasts reviews is not a growth strategy. It’s cosplay.

With that caveat clearly on the table, the new Ausha x Edison Research analysis of the UK’s Top 25 podcasts contains genuinely useful intelligence — if you read it correctly.

Ausha and Edison Research ran Edison’s Q1 2026 Top 25 UK Podcasts list through Ausha’s PSO Category Benchmark tool, analysing the 20 most recent episodes of each show on Apple Podcasts to extract the metadata and publishing patterns behind the UK’s highest-reach shows. Here’s what the data actually says.

On titles: The top UK shows average just 20 characters for show titles and 55 characters for episode titles – short, punchy, and built for recognition rather than search. Again: these shows don’t need to win a search result. They need their existing audience to find the new episode. That’s a different brief than growing a show from zero.

On publishing volume: The Top 25 UK podcasts release an average of 11 episodes per month, with a clear preference for mid-week releases. Wednesday is the single most popular publishing day, and Saturday publishing drops sharply — just 9 episodes across all 25 shows on a given Saturday, compared to 120 on Wednesday. The mid-week finding is consistent with other audience research: UK listeners are deep in their weekly podcast habits by Wednesday, and dropping content into that groove makes sense.

On episode length: The average episode across the Top 25 runs for 54 minutes, with the 30-minute to 1-hour window accounting for nearly 47.6% of all episodes analysed. But the range is striking — from under 10 minutes to over 2 hours, with more than a quarter of episodes running between one and two hours. Edison Research’s Gabriel Soto is direct about what the data means: there is no magic number. Format follows content, not convention.

On show descriptions: This area is where the study’s most useful insight lives — and it’s the one that pushes back hardest against imitation. The Top 25 shows average just 549 characters in their show descriptions. But Ausha’s own recommendation is to write at least 3,000 characters for podcasters looking to grow. The top shows can be brief because Apple’s algorithm already knows who they are. Everyone else needs to give the algorithm something to work with. PSO is how shows without brand recognition climb the rankings — but you can’t rely on PSO alone to achieve discovery with just a three-sentence description.

On social proof: The UK elite average a 4.5-star rating on Apple Podcasts and approximately 8,500 reviews per show. These numbers are useful as long-term targets. You cannot achieve these numbers by asking your audience just once. They’re the cumulative result of years of consistent listener relationships.

Source Note: This study was produced by Ausha, a podcast hosting and marketing platform with a direct commercial interest in promoting its PSO tools, in partnership with Edison Research, whose Top 25 UK Podcasts methodology is based on listener reach data. The analysis is limited to Apple Podcasts and covers only the 20 most recent episodes of each show at time of analysis. Findings reflect patterns among already-established, high-reach shows and should not be treated as prescriptive publishing rules for emerging podcasts. Ausha’s PSO recommendations within the study are explicitly promotional for its platform products.

The Key Points

Wednesday is the peak publishing day among the UK’s Top 25 podcasts, with 120 episodes dropped on Wednesdays versus just 9 on Saturdays — a mid-week strategy aligned with established listener habits

The average episode length is 54 minutes, with the 30-to-60-minute window accounting for nearly half of all episodes, but the format range spans from under 10 minutes to over 2 hours

Show titles average just 20 characters — a brand recognition strategy, not a discovery strategy, and one that only works for shows already at the top

The Top 25 average 8,500 Apple Podcasts reviews per show and a 4.5-star rating, reflecting the social proof infrastructure that reinforces algorithmic visibility over time

The metadata gap is the real finding: top shows use brief descriptions (549 characters on average) because they don’t need search to find them — growing shows need to do the opposite, with Ausha recommending a minimum of 3,000 characters for discoverability

Why It Matters

The UK podcast market is maturing fast — and the gap between the shows with institutional brand recognition and everyone else is growing. Studies like this one are valuable precisely because they expose that gap. The Top 25 can afford to be brief, inconsistent on length, and light on SEO because their audiences already know where to find them. For the thousands of UK shows trying to climb into that tier, the lesson isn’t to copy the habits of the elite. It’s to understand which habits reflect their success and which reflect their comfort. Publishing on Wednesday? Actionable. Writing a 549-character description? Trap.

The Big Picture

For podcasters: Wednesday releases and 30-to-60-minute episode windows are genuinely useful reference points — but they are starting positions, not rules. The most actionable finding in this entire study is the description length gap. If your show description is under 1,000 characters, you are handing back discoverability to Apple’s algorithm without giving it anything to index. Fix that first. Keyword-rich, detailed show descriptions cost nothing to write and are the single highest-leverage SEO move available to any podcast that isn’t already a household name.

For podcast producers: The publishing volume number deserves attention. Eleven episodes per month across the Top 25 means these shows are operating as content machines with dedicated production infrastructure — editors, schedulers, production managers. If a client is asking why their three-episodes-a-month indie show isn’t charting alongside the BBC and Global Radio, this data gives you the honest answer: at the top of the UK market, consistency and volume are table stakes. That’s a production investment conversation, not a strategy one.

For the industry: The co-commissioning of this study by a hosting platform is worth flagging — but so is the fact that the collaboration between a commercial tool vendor and an independent research organisation like Edison is becoming a standard model for podcast intelligence. The resulting data is useful. To Ausha’s credit, the caveats are stated rather than buried. What the industry needs now is the same analysis applied across markets – Australia, South-east Asia, North America – so publishers can compare UK patterns against regional norms rather than treating one market’s Top 25 as a universal playbook.

JOIN PODWIRE’S MARKETPLACE

If you’re building a podcast team, join Podwires Marketplace to access monthly curated lists of experienced podcast professionals—producers, audio engineers, scriptwriters, and hosts—actively seeking new opportunities in news, storytelling, and audio journalism.

If you’re a podcast professional seeking your next opportunity, join the PodWires talent directory to connect with podcast companies and media organisations.

🚨 Stay on top of your deadlines with our weekly-updated calendar of fellowships, grants, training opportunities and podcasting events. If your organisation has a fellowship, grant or event to share, just 👉 fill out this form or 👉 reply to this message.

INTRODUCING PODWIRES TOOLBOX

Discover the tools podcasters actually use. Explore Podtoolbox to find trusted software, services, and resources to help you plan, produce, grow, and monetise. Indicate that the framework is already obsolete, rather than your podcast. monetise

Explore podcast tools for every stage of growth, or add your own to the directory.

THAT’S WRAP

SPONSOR US

Reach over 1000 podcast producers with your product.

Thousands of podcast producers, audio/video editors, podcasters, executives, and business owners worldwide read our newsletter. Contact us now.

📖 I appreciate you taking the time to read! See you in the next issue. Got a question or criticism? Just click on Reply. We can talk while we are here.

Please provide a press release along with a suitable landscape photo. Make sure it’s newsworthy. Send press releases to editor@podwires.com or click here. Editorially, we may rewrite headlines and descriptions.

📬 Sponsor us and get your brand in front of thousands of independent podcast producers and podcasters. Email us at sales@podwires.com for more information or as personal supporters via Patreon, as your contributions help us enhance the experiences of all our users.

🖊️We are delighted to hear from our subscribers! If our newsletter helped you or you have a success story, we would love to publish your testimonial. 👉 Post a Testimonial: Click here

🚀 We are here to help you succeed! We kindly invite you to complete a brief 5-minute survey to share more about your business and yourself. These questions will help us better understand you and promote your business as part of our mission. It’s a win-win!

🚨 Did someone forward the information to you?

Become one of the more than 1000 valued email subscribers. Find Out More 👈

We’d love to share what our Podwires readers have been saying!

We’re so grateful to our previous Podwires advertisers!

Podwires is here because of our incredible partners’ unwavering support. The Podwires readers receive journalism free of financial and political influence. If you found this valuable, consider Restacking so more people can see it. Get together with them today.